Your Custom Text Here

The shape of a “yes”

When someone evaluates a new product, they are not evaluating the product in the abstract; they are evaluating a distribution of outcomes. This may happen consciously or subconsciously, but especially in B2B there is no universe in which it doesn’t happen.

A buyer will routinely cycle through a series of questions as they attempt to model out the payoff structure your product may produce: how large is the perceived upside? How quickly does it arrive? What is the shape of the perceived downside, and how reversible is it?

Putting the answers to these questions together produces a payoff curve. The shape of that curve decides whether your product gets adopted or whether it gets a “come back next quarter,” which is where B2B startups usually go to die.

You almost always want to be selling capped downside for material upside. Conversely, you want to stay away from unlimited downside for marginal upside. This sounds obvious, but it gets missed all the time. What matters here is not what the founder believes the payoff curve looks like, but what the buyer believes, or is likely to believe. That is worth modeling deliberately while building the product because it changes the product itself. Better engineering, better feature selection, better pricing, compliance work, and channel choice can all improve the shape of the curve.

This is not as simple as it sounds. You need to correctly identify the buyer, understand the constraint space they operate in, their risk tolerance, and the kinds of upside that matter to them. Mid-market CFOs, for example, are infinitely more risk-averse than startup founders. If you hallucinate those things, you will spend at least a couple cycles selling the wrong product to the wrong people. Get them right, and you may “pass go.”

A product can create real value and still present a bad curve to the buyer. This happens constantly in B2B. The founder may see time saved, cost reduced, throughput increased, revenue unlocked, where the buyer actually sees implementation burden, trust risk, internal scrutiny, and personal downside. Only one of those world models matters.

A lot of products create value. Fewer create a proposition the buyer can safely say yes to. That is why buyer identity matters so much. Who they are, what they optimize for, what they get rewarded for, whether they are a principal or an agent, how legible the upside is to the rest of the organization, how much of the downside lands directly on them, and so on.

Further, distribution directly influences the shape of the curve. Take the example of a young company proposing a new capability to a risk-averse buyer. While a genuine value-add, there are few comparables in the marketplace. The buyer models the curve, usually with some loss, and decides that their company gets most of the upside if things go well, while they carry most of the downside if they don’t. That is a bad curve: some bounded operational upside against personal, reputational, and career risk. “Nobody gets fired for buying IBM.”

Now take the same underlying capability and offer it as infrastructure to a platform that already serves that same buyer. The platform can unlock a new capability for its customers, expand into new regions or user segments, improve its margins, or even open a new revenue line. By the time the value proposition reaches the end user, it comes from someone they already trust, bundled with other value they already consume. It proposes an enhancement to a shape they already understand, rather than asking them to fit a wholly new shape into their operating model, which consequently improves your adoption odds.

So by this token, startups often fail because they present products with poorly constructed payoff curves to the wrong buyers. It is certainly not the only way to die as an early-stage startup; there are plenty of those. But this is a fairly common failure mode, especially early on. The product may work. The capability may be real. The value may even be obvious to the founder. But that is not enough.

What matters is the shape of the payoff curve as it is understood by the buyer.

Applied Science for early-stage founders

Preface: This is not a new planning system, nor a founder playbook. There’s no shortage of great tactical frameworks out there. The aim here is narrower and upstream: to name the epistemic standard that determines whether any system (OKRs, sprints, chapters, Linear workflows) is producing truth, or merely producing motion.

In other words: how do you know you’re learning, rather than getting better at narrating what you’re already doing?

Early-stage companies don’t fail from lack of effort. They fail from undisciplined belief. When feedback is weak the mind fills in the gaps with narrative. If you don’t build a mechanism that consistently smokes reality out of its bear-cave, you end up mistaking motion for progress.

Rated taught me a valuable lesson across every era of the journey: time in business is not neutral. It either works for you, or against you. It either compounds your decisions, or compounds your mistakes. It is a loaded revolver, and if you’re not holding it, you’re sitting in front of it. There is no version of reality where the gun isn’t there. There’s no “neutral” state for time.

As first-time founders, we often told ourselves we were being rigorous. We stayed on a default path while waiting for more data before making the hard call. “Just one more month of data, bro, I promise.” Weeks would often became months, and the company, while still moving, softened at the edges. Decision drift did quiet damage, the kind you only recognize down the line unless you’ve learned to notice it early.

Some time after the initial adrenaline had worn out, and before anything felt inevitable, I internalized the real job description. Ken Griffin has a blunt line that captures it well:

“You’re constantly making decisions under uncertainty. That is the job.”

Once you see that, you can’t unsee it. The founder’s calendar is not a schedule of work. It’s a schedule of decisions.

Around that period, I started treating early-stage as applied science. I began using decisions as the pacemaker by flipping the relationship between time and decision-making. Instead of letting time pass in the hope that more data would eventually make the decision easier, I made the decision itself the unit of time.

Concretely, that means organizing the operating rhythm of the company around decision intervals. Every two weeks, a decision is due. The checkpoints go on the calendar and recur. That constraint forces compression: you plan and execute inside the interval in a way that produces high-density evidence for the decision at the gate.

The goal is to put yourself and your team in a position to make good decisions at a steady clip, and fast enough to earn survival before you run out of money. There’s an adjacent point here about why over-raising before PMF can dull this muscle, but that’s a separate note.

Done well, it forces focus, cuts scope creep, and improves sleep because uncertainty gets a clock. You stop waiting for clarity. You set a decision date, then do the work that earns it.

This post is the operating system behind that approach.

A founder-friendly definition of “Applied Science”

For founders, applying “science” is how you ensure you stay honest and rigorous when the signal gets noisy (hint: it’s almost always noisy).

In early-stage work, the most common failure mode is when you start using motion as evidence, and “we built it” as “we learned something.” Applied Science is the reverse. It asks for three things before you begin:

You name the hypothesis you’re trying to validate.

You define the instruments that will collect reality.

You define rules that make “keep going” earn its keep, ex ante.

Nothing in this operating system is invented from scratch. It borrows heavily from Lean Startup’s experimental posture and Shape Up’s timeboxed execution, but is different in a couple key vectors that make it particularly effective in an early-stage environment.

The “Lean Startup” is an experimentation mindset: it teaches you to treat ideas as hypotheses, get out of the building, and iterate through build–measure–learn cycles, while minimizing waste. What it doesn’t give you is enforcement. It’s easy to “keep learning” forever, while avoiding the moment where uncertainty has to collapse into a decision.

“Shape Up” is an execution container: it timeboxes work, forces scope discipline, and creates space for teams to ship coherent products without endless backlog churn. What it doesn’t give you is a pathfinding grammar. It’s excellent when you already have a direction and you want to ship coherent work; it’s less explicit about how to design experiments, what constitutes disconfirming evidence, and when the right move is to kill the direction rather than re-scope the work.

The “Applied Science” approach borrows from both, but it’s aimed at a different failure mode: decision drift under weak feedback. It makes the decision cadence explicit. You schedule the decision threshold first, then build the instruments that force reality to answer before the deadline, with pass/fail criteria set up front.

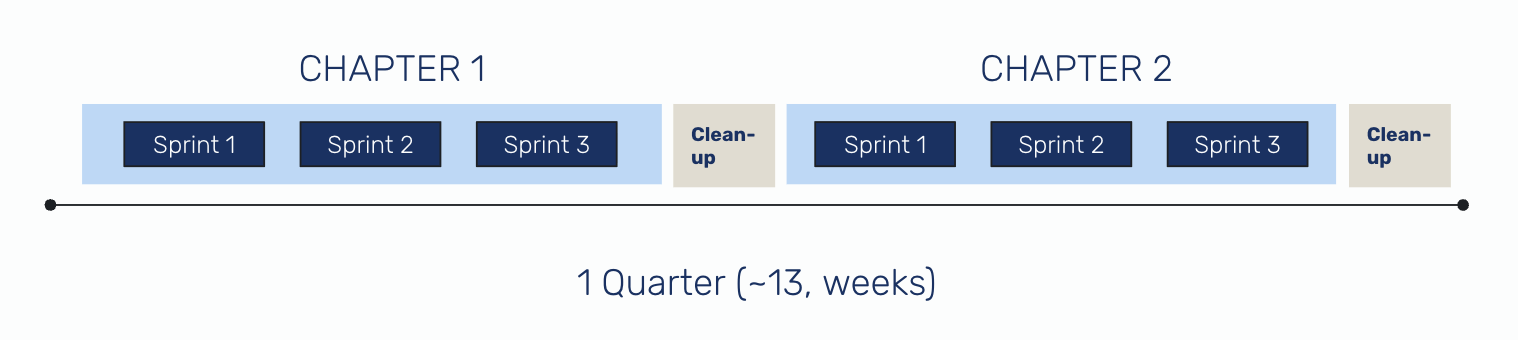

A quarter split in Chapters and Sprints

The container: Chapters

Work in the Applied Science framework happens in 6-week cycles I call Chapters.

A Chapter is a strategic container with a single governing direction, expressed as a master hypothesis. Sometimes that hypothesis is market-facing: a belief about buyers, urgency, and adoption that must hold for the company to work. Sometimes it’s technical: a belief about what you can actually build, and what it will cost in complexity, reliability, and time.

In principle, one Chapter should hold one master hypothesis. In practice, depending on resources and maturity, you can sometimes carry two, but rarely more. The cleanest version of “two” is when you’re straddling two distinct uncertainties: a go-to-market question and a build question. Will anyone buy this, with these constraints, at this price? And can we actually build the minimum surface area required to test that purchase intent without turning the company into a science project?

Earlier than that, the question often isn’t “will they buy” yet. It’s “what form of this idea is legible to the market today.” You’re searching for a wedge the market can immediately read: a concrete workflow they’ll delegate and a proof point that makes it feel safe.

Six weeks is long enough to build something real, and short enough to keep you honest. That’s the practical reason Chapters are six weeks.

The more important reason is decision cadence. A Chapter creates a date where you have to decide. It cuts off the endless “one more iteration” loop and gives you a temporal boundary your brain can’t negotiate with. The operating rule inside a Chapter is fixed time, variable scope. If the work is too heavy, you don’t negotiate the deadline, you cut scope.

The point of a Chapter isn’t to ship a lot. It’s to run the highest-quality sequence of experiments you can fit into six weeks, so you can make a real decision when the Chapter ends. You start with the master hypothesis, then design a chain: each experiment reduces a key uncertainty, and earlier results shape what you do next.

One Chapter might be market-heavy: build a demo that makes the value concrete, show it to fifteen target buyers, and test a few ICP slices to see where urgency and willingness to change behavior concentrates fastest. Another might be technical: prove you can execute the core workflow end-to-end under real constraints.

In market Chapters, the outputs aren’t “we built a demo.” They’re patterns: which ICP leaned in, which language triggered recognition, which objections repeated, and what the buyer asked for next.

In technical Chapters, the outputs aren’t “it works.” They’re failure modes, reliability costs, and whether the architecture is converging toward something you should commit to for another Chapter.

The heartbeat: Sprints

Inside a Chapter, there are three 2-week Sprints.

Sprints are tactical containers. Their job is to turn experiment design into execution. Chapters decide what we’re trying to learn by a deadline. Sprints decide what we’ll do in the next two weeks to force reality to answer. Each Sprint begins by turning an experiment into a protocol: who we’ll test with, what we’ll ship, what we’ll measure, and what would count as a pass or fail. Then we run it.

Every Sprint must ship something that moves you closer to proving or disproving the Chapter hypothesis.

You pick one or two experiments, then write a simple protocol: what you’re testing, how you’ll test it, who you’ll test it on, and what would count as a pass or fail. You also name the artifact you expect at the end. This could be a demo app, a workflow spec, an ICP map, a “why now” narrative doc, etc. Artifacts turn learning into memory. Without artifacts, teams “learn” the same lessons repeatedly because nothing gets carried forward.

Then you execute. The Sprint plan is the contract. New ideas are noted, but they wait until the next boundary. That’s the cadence doing its job: focus during the Sprint, creativity at the edges.

Every Sprint ends with synthesis. You answer four questions in plain language: what did we observe, what did it imply about the master hypothesis, what surprised us, and what decision does it force about the next Sprint’s experiment slate.

If you’re doing market work, synthesis looks like patterns in objections, language that reliably triggers recognition, and whether the buyer took the next step without being dragged. If you’re doing technical work, synthesis looks like failure modes, reliability costs, and whether the architecture is converging or expanding.

There’s also a social purpose here. Collaboration is highest leverage at the boundaries and tends to become noise in the middle. So Sprints deliberately alternate between intense alignment and quiet throughput. The team gets long, uninterrupted stretches to build and run experiments. You still move fast, but it’s a calmer speed: fewer meetings, fewer reopened debates, fewer half-decisions.

Chapters end in decisions. Sprints produce the evidence.

Outcome-based Kill Gates

Kill Gates are the pass/fail criteria you set at the beginning of a Chapter. They exist at two levels: they gate Sprints, and settle Chapters.

This is where the system stops being a cadence and becomes applied science. Kill Gates are defined up front, during Chapter shaping and Sprint planning. Start with the hypothesis (master or child), describe what success would look like by the end of the Sprint or Chapter, and then invert it. The inversion is the Kill Gate: if the world fails to look like this by a specific time, we stop treating the hypothesis as alive.

A Kill Gate is the moment you ask: did we earn the right to run the next experiment in the chain?

A good Chapter has three or four Kill Gates. Not twenty. They should be legible, falsifiable, and tied to the uncertainties that matter. They do two jobs. They prevent narrative, and force focus. Once the Kill Gates are clear, you work backwards: which experiments produce evidence for or against each gate, and what artifacts must exist by the end of each Sprint for us to meet the gate?

That’s how Kill Gates connect to Sprints. Each Sprint ends with a gate-check. Clear the gate and you advance. Trip it and you change something while there’s still time: the experiment design, the population, the product tilt, or the hypothesis itself.

At the Chapter level, Kill Gates become the decision mechanism. You evaluate against the gates you defined at the start. As a default heuristic, if two of four gates are not met, treat the direction as compromised and reconsider the approach. If three are tripped, pause and evaluate whether the governing direction should be killed rather than rehabilitated.

A lot of the time, the decision should come in the shape of: “commit another Chapter to this direction,” which is a very different statement than “we’re building this.” Sometimes it’s “narrow to this ICP,” or “the workflow is right but the control surface isn’t,” or “this hypothesis is dead.” Once you decide, you work backwards again: what evidence would make the next decision obvious, and what experiments belong in the next Chapter?

The point is to preserve interpretability and time. Kill Gates turn six weeks into a controlled experiment with stopping rules. They force a decision, and they make the next Chapter easier to design because your work is systematic, not vibes-driven.

Startups are a stacked tower of risks: market, product, distribution, technical, regulatory and so on. Progress is retiring risks in the right order. Chapters choose which layer you’re trying to de-risk next. Kill Gates keep you from building higher while the base is still moving.

The Clean-up Week

Between two Chapters, there is a Clean-up Week.

This week exists because well-run Chapters are intense. They compress effort, they pull you into tight execution, and they generate a surprising amount of data (e.g. customer reactions, edge cases, failure modes, pricing signals, objections). In the middle of a Sprint you rarely have the cognitive bandwidth to let any of it sit. You’re collecting reality faster than you can process it.

Clean-up Weeks are the deliberate step back that helps you turn raw data into concrete understanding. Different people assimilate at different speeds, but everyone benefits from leaving the frame of focused execution and giving the mind some quiet time to connect dots. The useful synthesis often arrives when you stop pushing and allow the evidence to settle. Stare at the wall, take long walks, reread the notes with fresh eyes, and notice what repeats. That’s not indulgence. It’s part of the method.

A well run Chapter should produce a strong result that becomes a building block in your mental model for the company. At the closing point, you stop doubting the validity of the finding and build upwards from that checkpoint without looking back. It should take very strong disconfirming evidence for you to re-litigate the findings of a well run Chapter. Hence, it’s extremely valuable to not only run a Chapter well, but also to process the findings well.

The week still has practical outputs. You close small loops that would otherwise accumulate into drag: reliability footguns, obvious debt. You convert learnings into artifacts the team can carry: a short Chapter write-up, updated hypotheses, refreshed Kill Gates, and a clearer map of what changed your mind. And you shape the next Chapter just enough that Sprint 1 begins with clarity.

Without this week, Chapters blur. You carry residue forward, and the Applied Science OS degrades into one continuous smear of half-finished work and half-made decisions. With it, each Chapter stays discrete: experiment, verdict, reset, then the next attempt.

Boundary conditions: keeping your bearings straight

At this point, it’s essential to note that not everything is under test all at once.

Chapters and Sprints exist under a mission umbrella. The mission is the boundary condition. It defines the direction of travel, not the exact path.

“To accelerate the world’s transition to sustainable energy.” - Tesla

“To be Earth’s most customer-centric company.” - Amazon

“To increase the GDP of the internet.” - Stripe

Notice that none of the above talk about how they will achieve the mission. They don’t name a wedge, a product, a channel, or a planning cadence. They state an invariant, then allow the implementation to evolve over time. The shape of the mountaintop should be clear; which face of the mountain you start climbing, or the one you pick to get to the next basecamp, are the variables.

You touch mission and vision only if repeated Chapters fail. Chapters are not about re-deciding why you exist.

A Chapter is a falsification container for a specific hypothesis at the current level of resolution. Tactically, it might be: will anyone pay for this in its current form? If the answer is no, the goal is to generate enough evidence in six weeks that you stop reopening that question. That new prior becomes stable. It becomes part of your world model. The next Chapter is not a new identity. It is the next best hypothesis for how to move toward the same mission.

Operating the lab: leader and team, as one system

In early-stage work, “leadership” can’t mean distance from the work. The job is closer to running a lab than running an org chart. Someone has to protect the cadence, force decisions on schedule, and keep the team oriented around the same hypothesis. Call that person the editor, the lab lead, the dungeon master.

Their core responsibility is epistemic hygiene: shaping the Chapter, hosting the hard debates at the boundaries, collating evidence as it comes in, and breaking ties when the system produces ambiguity.

That doesn’t mean they’re in an ivory tower. They still produce data wherever they’re highest leverage: customer conversations, demos, synthesis, writing, sales experiments, instrument design, unblocking. The difference is that their involvement serves the experiment, not their ego. They participate in the work while also guarding the frame the work lives inside.

The team’s role is to take a fuzzy question and make it testable. They own chunks of the work end-to-end: turn a hypothesis into something you can actually put in front of the world, run it, and capture what happened in a form the team can reuse. Concretely, that might mean: building the demo and writing the script; finding ten target buyers and running the calls; shipping a workflow slice behind a feature flag; adding the one metric that tells you whether the workflow is being used, and so on.

Just as importantly, the team owns synthesis. They don’t report activity. They compress what happened into the handful of patterns that matter: what repeated, what surprised us, what changed our mind, and what we should do next.

One emergent property of operating this way is that you need less “management.” Context becomes shared because shaping is a product of debate, not a decree. Success and failure are legible because Kill Gates are defined up front. The direction stays coherent because the Chapter is a single governing hypothesis with a deadline.

That clarity makes ownership easier: people can take a slice of the experiment and drive it end-to-end without constant check-ins, because they know what they’re solving for, how it will be judged, and why it matters.

Shots at the bat: time measured in Chapters

One of the biggest benefits of this system is that it changes how you perceive time.

“Eighteen months of runway” feels like space. It reads like optionality. It invites softness.

“Eight Chapters of runway” feels like physics.

Chapters are discrete attempts to retire risk, and the moment you start counting your remaining attempts, the work becomes more honest.

The other reason the framing bites is that progress isn’t monotonic. You can’t expect that you will keep moving in a straight line up-and-to-the-right, without interruptions.

In reality, you sometimes discover something terminal higher up the stack and you have to revisit the foundation. The wedge isn’t legible. The distribution channel doesn’t work. The technical approach is too brittle. You don’t just “iterate.” You reset the stack hypotheses, which effectively burns a Chapter without moving the tower upward.

That’s why months can be misleading. Months pretend you move linearly. You do not. You move step-wise.

This also forces a more forthright relationship with fundraising timelines. It’s common to say, “we have runway until X.” A sharper question is: how many Chapters do we have before we must raise, and how many of those Chapters are realistically productive given the probability of resets? If you think you have four Chapters left before a raise, you start acting like every Chapter is one of your remaining shots.

Chapters and long-range planning

Over time, the Applied Science framework becomes a practical way to do long-range planning without reverting to bottom-up roadmaps, which are often more performance art and less planning artifacts.

You still set a destination (e.g. ten months from now we want ten customers, a credible revenue run rate, repeatable conversion, a proof point that makes the next round legible), and then work backwards in Chapters. What risks must be retired, in what order, to make those milestones plausible? Which Chapters are for legibility (wedge + ICP), which are for repeatability (distribution + conversion), which are for robustness (reliability + controls), and which are for scale (expansion + pricing + onboarding)? And how are they appropriately sequenced so that we can reduce churn in our progress?

Once you accept that Chapters are finite attempts, redundancy becomes expensive in a way months don’t capture. Doing something in Chapter 1 that only becomes meaningful in Chapter 5 isn’t “being proactive.” It’s burning an attempt before the upstream prerequisites exist. That’s six weeks of runway converted into churn.

So the planning problem becomes sequencing. You want the outputs of one Chapter to become the prerequisites for the next. Respect dependencies and you avoid rework; the same logic as not building the first floor before you’ve poured the foundation.

Practically, this means you front-load the most foundational uncertainties and delay anything that depends on them. You don’t polish onboarding before you’ve found a wedge that people will adopt. You don’t scale outbound before you have language that reliably triggers recognition. You don’t harden infrastructure before you know which workflow you’re committing to. You don’t design enterprise controls before you’ve proven anyone will delegate the action at all.

Then, as you retire risks, the “next stack” becomes visible. Early on you’re mostly de-risking legibility and feasibility. Later you’re de-risking repeatability: distribution, conversion, retention, operational reliability. Later still: unit economics, compliance posture, scale constraints.

Each layer changes what experiments are even worth running.

Why this matters beyond productivity

This system isn’t just about being organized. It’s also about staying sane.

Early-stage operating comes loaded with prolonged exposure to ambiguity. Your nervous system keeps trying to close loops that reality won’t close yet. In that vacuum, the mind manufactures narratives. You can work sixteen-hour days and still feel behind, because “ahead” is undefined.

A decision cadence turns ambiguity into discrete questions with deadlines. It turns existential dread into a finite number of Chapters. It gives your brain permission to stop spinning, because it knows when the next verdict will happen and what evidence will count. It gives you a way to be both intense and calm.

There’s also a tempo effect. When collaboration is concentrated at boundaries and execution is protected in the middle, the work becomes smoother. And smooth becomes fast, because you’re not paying the hidden tax of re-litigation, context loss, and perpetual half-decisions.

Most importantly, it makes failure cheap. A failed Chapter is an experiment that returned a negative result, not a personal indictment about your quality as a builder. You move to the next Chapter with less shame and more information.

Closing

If you’re early-stage and you feel like you’re working constantly yet not moving, there’s a decent chance the problem is not effort, but decision structure. You’re letting the calendar drift and paying for uncertainty with narrative.

Set a decision you must make on a date. Build only what produces the evidence for that decision. Pre-commit to the outcomes that kill the idea. Repeat.

That’s the whole method.

And once you install it, you start to notice that the company stops feeling like a fog, and starts feeling like a sequence of crisp questions you can answer.

You are not standing in front of the gun. You are holding the gun.

___

We’re running this OS right now in a project that will go unnamed for now. It’s improved speed, decision quality, and wellbeing, without sacrificing intensity. If you adopt any part of it, send me the sharp edges: where it failed, what was gameable, and what you had to modify.

Language is executable

Lived reality is a mess of biological signals that oscillate between fear, ambition, fatigue, desire for status. Too much, too fast, and mostly without structure. The human mind cannot work directly on this raw feed. It needs compression.

Language provides that compression.

In human systems, words are not merely labels applied after the fact. They are executables: scripts that instruct the mind how to construct experience, often through second-order effects rather than literal meaning. They determine what counts as a problem, what feels urgent, what can be ignored, and what action becomes available.

When you feed a specific word into a human mind, you are not describing reality; you are writing a line of code. If you write, “This is a Dashboard,” the code triggers a subroutine called work. If you write, “This is an Assistant,” the code triggers a subroutine called relief. The underlying system is identical, but the compiled experience is not.

That’s because conscious experience does not operate on raw input, but on symbols: a threat, a deadline, this is progress, I’m failing, that’s a chair. It compiles before it evaluates.

Evaluation assumes you can step back, look at a thing, and decide what it means. Compilation is more primitive. The input is executed before it is judged. By the time evaluation occurs, the program is already running.

By that token, words do not passively sit on top of experience. They decide what the mind notices, what it ignores, what feels urgent, and what feels optional.

In the physical world, language has no write-access to reality. Call a broken chair a "throne" and it still collapses under load. But in the realm of ideas (e.g. software, markets, organizations) language has root access. There is no physical substrate constraining the ontology of concepts. “Problem” routes the mind toward stress and remediation. “Puzzle” routes it toward curiosity and play. Same situation, radically different experience rendered.

In markets, this re-labeling creates billions in value. If you call it "letting strangers sleep in your spare room," it is a safety risk. Call it "The Sharing Economy," it becomes a movement.

The same logic applies recursively to your own psychology. We are constantly running a source code, often without debugging it.

When abstractions are wrong you get identity erosion, status mismatch, or motivational leakage. Get the abstractions right, and you restore coherence, pride, and decisiveness. All the while, your life and coordinates haven’t moved an inch.

Take an engineering organization. Frame a project as “technical debt cleanup,” and it produces motivational leakage; it feels like taking out the trash. Frame the same work as “platform hardening,” and it produces identity reinforcement; it feels like preparing a fortress for battle.

Human cognition is thresholded. Understanding does not always accumulate gradually, and it often arrives all at once; "it clicks." That click is the compiler resolving dependencies. It’s you importing the right library.

LLMs have pulled this dynamic into the foreground. We can now observe language and its effects in real time.

For most of history, the effects of language were diffused through slow, noisy human systems. You said something. Time passed. Outcomes shifted (or didn’t). The distance between words and consequences was often either long enough to remain ambiguous, or too costly to test in the moment.

With LLMs that distance has collapsed.

You write a prompt. You change a few words. The output changes immediately—sometimes dramatically—while everything else remains constant. Same system. Same capabilities. Different instruction.

The same mechanism operates in human communication, whether written or spoken. What’s striking is not that it works this way, but how rarely we notice it.

A warning is required. Language can clarify reality, but it can also distort it. When an abstraction invokes capabilities that the underlying reality cannot sustain, the system eventually rejects it. Energy turns into friction. Coherence collapses.

Whether you are naming a feature, aligning a team, or narrating your own day, you are writing source code.

Your words are not commentary. They are instructions.

Interfaces for intention

For most of history, expertise was held hostage by friction. To make a contribution, you had to navigate the toolchain: the arcane workflows of finance, the rigid protocols of healthcare, the compiling errors of engineering. The interface acted as a gatekeeper. You had to pay a tax in "machinery" before you could transact in "ideas."

AI decouples mastery from the machine. As the cost of turning intent into execution tends toward zero, the interface stops absorbing the difficulty. The bottleneck moves upstream. When procedural fluency is no longer the constraint, the scarce resource becomes structural awareness: the ability to articulate what should happen, under which constraints, and with what consequences.

Skill stops being about technique. It becomes about specification.

This creates an interface crisis. If expertise is now "intention shaped by constraints," where do we type that in?

The current consensus is "Chat." Chat was the first surface AI unlocked, and it is excellent for exploration. It lowers inhibition and widens the search space. But Chat is a low-fidelity medium for architecture.

Chat captures desire, but not boundaries.

It has breadth, but no topology.

It is stateless in a world that requires state.

You cannot build a complex system in a text box for the same reason you cannot build a skyscraper using only oral instructions. A world where intent moves in lockstep with execution requires a surface where structure is visible. An interface where constraints are explicit, flows are legible, and feedback loops are closed before execution is locked.

We need an IDE for strategy.

We have seen this shift before. In the 1980s, the spreadsheet collapsed the machinery of finance into a 2D grid. Suddenly, the structure of a business became legible and malleable. People who had never touched a mainframe could model levers, run scenarios, and debug logic. Marketers built forecasts. Operators ran capacity plans. The "Machinery Tax" vanished, and the value of pure reasoning skyrocketed. The result was cross-pollination. Reasoning developed in one corner of an organization could travel to another because the primitive (the cell) was universal.

We are standing at a similar threshold. The frontier is not "better models." The frontier is the meta-interface that allows us to compose these models.

When machinery is no longer the barrier, the transferable part of expertise becomes a person’s mental models. The penalty for stepping into adjacent fields drops.

Unlocking the next layer of value requires a medium that respects the shape of complex problems, not just their semantic content. Until we build the interface that turns 'Chat' into 'Architecture,' we remain stuck at the command line of a new era.

The second derivative of conflict resolution

I wrote this after noticing a pattern in how good teams and good relationships evolve. It’s not that they avoid conflict, but rather they metabolize it faster every time. The model that emerged was a mathematical one; relationships as learning systems, their health measurable by the slope of repair.

One of the beliefs I hold most firmly is that the best predictor of success in any relationship, whether romantic, friendship, or team, is the second derivative of conflict resolution.

By conflict, I don’t mean shouting or drama. I mean any point where expectations diverge and two internal models of reality collide.

A great relationship is not one without friction; it’s one where friction resolves faster and cleaner over time. The first time you face conflict, it takes a day to recover. The second, six hours. The third, ninety minutes. The fourth, twenty. After that, the curve asymptotes toward zero.

That curve, the rate at which repair accelerates, is what I call the second derivative of conflict resolution (SDCF). It measures not harmony, but learning. Every disagreement, once resolved, adds a building block to shared understanding, which means you don’t have to fight the same fight twice.

This reframes relationship quality from being about harmony to being about adaptive efficiency. The first derivative of conflict resolution shows how quickly a single conflict resolves (i.e. the velocity of recovery). The second derivative shows how that velocity improves over time (i.e. whether the system learns). In simpler terms, what matters isn’t how fast you repair once, but how fast you get better at repairing.

If over successive conflicts the first derivative (recovery speed) becomes more negative more quickly, meaning repair happens faster each time, then the second derivative across conflicts is positive in the direction of learning. Conversely, when the second derivative flattens or turns negative (i.e.when conflicts take just as long, or longer, to resolve) it’s a sign of structural incompatibility. The system isn’t learning. What looks like “communication problems” is really the absence of adaptation.

Most people assess relationships based on emotional tenor; how good they feel or how frequently they argue. But the SDCF model suggests something different; conflict isn’t a sign of failure, but rather it is signal. Each disagreement surfaces new data about boundaries, needs, and blind spots.

In that sense, the counterintuitive truth is that the path to relational strength runs straight through conflict.

Every repair is a form of learning; every argument, a test of how well two people can turn friction into shared understanding. What ultimately defines longevity is how efficiently that learning compounds, and how each conflict leaves the system slightly more aligned than before.

What we often call being “well-matched” is really just phase alignment under low stress. A relationship that truly compounds is one where both people elevate each other through conflict.

Common sense suggests compatible people should recover faster, but the inverse is also true; people who recover faster become more compatible. The variable you can actually control is the learning rate; the slope of repair.

It’s worth highlighting that awareness itself changes the shape of the curve. Most relationships operate unconsciously along their derivative, unaware of whether repair is accelerating or stalling. But once you can see the curve, you can influence it. Awareness reigns in entropy, and replaces drift with structure.

That awareness can have two outcomes, both good. It can either help a relationship move to a higher level of coherence, or reveal that the system has reached its limit, that its slope will never meaningfully improve, and thus allow it to end cleanly. Both outcomes are infinitely better than unconscious decay.

This lens changes how you think about relational “success.” It’s not about avoiding arguments or achieving constant peace. It’s about whether repair gets faster and deeper each time. Whether the feedback loop between conflict and understanding tightens. Whether the relationship compounds.

It also applies beyond the personal. Teams, partnerships, and organizations all have a SDCF. The best companies aren’t those without disagreement but those whose disagreement resolution curve steepens with time, as they learn to metabolize tension into clarity.

A team’s greatness isn’t its lack of internal debate, but how fast it integrates disagreement into improved operating norms. Cultures that avoid conflict decay, while cultures that metabolize it evolve.

If you believe this, then conflict stops being something to fear. It becomes diagnostic. You run toward it, because every repair is a data point on the curve. A chance to move the derivative in the right direction.

That, to me, is what separates fragile from enduring systems, whether personal or collective.

It’s not how they avoid stress, but how quickly and gracefully they repair after it.

Coase in the age of code

Updated in March 2026

In 1937, Ronald Coase asked a question that still pertinent today: Why do firms exist at all?

The answer felt settled for decades. Coase explained that firms emerge because the market is costly. Contracts take time, negotiations add friction, and information is imperfect. When it becomes cheaper to manage people internally than to transact externally, a firm is born. The invisible boundary of the firm lies exactly where these two costs meet.

I spent the last decade in the trenches of blockchains, DAOs, and “trustless” systems. Crypto’s grand promise was to eliminate the very frictions that gave birth to the firm; to replace bureaucracy with code, management with incentives, and contracts with consensus. The thesis was elegant: If transaction costs drop to zero, the firm should dissolve into the network.

That was the dream. But it didn’t happen.

Crypto solved less than it claimed because transaction costs were never the only reason firms existed. The deeper constraint was comprehension. Someone still had to decide what mattered, what was true, what to prioritize, what to ignore, and who was accountable when the system failed.

When you replace contracts with smart contracts, you still need judgment: what counts as a valid state, what to upgrade, when to fork. When you remove hierarchy, you rediscover governance, only now it’s slower, noisier, and happening in public.

Bounded rationality didn’t vanish with blockchains. It simply migrated to Discord. The same cognitive limits that once defined the borders of the firm now define the borders of the network.

Agency problems persist too. Token holders delegate to committees, multisigs, or core teams. Power concentrates. Decision-making slows. Coordination becomes its own cost center. Every “decentralized” organization ends up rebuilding a managerial layer; sometimes reluctantly, sometimes accidentally.

The irony is that Coase’s logic still applies, but the variables have changed. Coase saw transaction costs as economic. What he couldn’t see from 1930s London was that the true constraint on coordination is not contract enforcement, but comprehension.

A modern firm isn’t just a bundle of contracts; it is a bundle of cognition. Its size is limited not by the cost of managing people, but by the bandwidth of shared understanding. Technology lowers the cost of transaction, but it does not raise the ceiling of comprehension. We can move money instantly, but aligning meaning still takes time.

This is the paradox of the digital firm: Infinite speed. Finite sensemaking.

AI now attacks the problem more directly. If crypto tried to replace trust, AI tries to replace hierarchy. The old managerial layer existed partly to route information: summarize context, resolve ambiguity, escalate decisions, and keep the organization coherent. In an AI-native company, much of that routing can be done by software.

This makes the firm smaller, but not obsolete. It removes some coordination cost, but it does not remove judgment cost.

Even if code can settle value instantly, humans still need slower systems for context, accountability, and trust. The firm endures because it optimizes for judgment, not just execution. This is why DAOs still look suspiciously like companies. They route capital through tokens, but their structure (small cores, delegated authority, bottlenecks) echoes the same patterns Coase described. It turns out coordination is a harder problem than trust.

What has changed is the granularity. The minimum viable firm used to require offices, payroll, management layers, and legal scaffolding. Now it can exist as a wallet, a passkey, a group chat, and an intelligence layer that keeps the context alive.

This does not end the firm; it distills it.

Coase explained why we built firms.

Crypto showed that trust could be programmed.

AI is now testing whether coordination can be compressed.

What remains is the irreducible core: judgment, accountability, and a shared reason-to-be.

The firm is not disappearing. It is being reduced to what only humans can still hold.

When smart people fail together

In every financial crisis, billions are lost not by crooks, but by smart people doing honest work, usually inside a committee.

We assume that adding high-IQ people to a room increases the group’s intelligence. Often, it merely amplifies the noise. A committee is not a social gathering; it is a signal processing unit. Its output depends entirely on its architecture. If the logic gates are faulty, more input just creates more error.

In systems theory, "Groupthink" isn't just people agreeing with each other; it is correlated error. When five people make the same mistake for the same reason, you don't have five data points. You have one data point, five times louder. A healthy system requires uncorrelated error. You want diverse pairs of eyes on the same truth, so that individual biases cancel each other out rather than compound.

This requires a shared epistemology. Most groups fail because they are arguing over the output (the decision) without agreeing on the source code (the method).

How much evidence is “enough”?

What is the logic of the tie-break: empiricism or first principles?

What is the protocol for falsification?

Without a shared operating system, collaboration becomes friction. You get "consensus," but consensus is rarely truth. Consensus is just the point where everyone’s fatigue exceeds their conviction.

Consensus should exist only at the level of the protocol. Beyond that, the goal is not agreement; it is accuracy.

We treat cognitive biases (anchoring, sunk cost, scarcity) as personal failings. They are not. They are recurring bugs in the human firmware. You cannot "train" them out of individuals, any more than you can train a computer to stop doing exactly what its code says. You can only build a system that traps them. You need a "Garbage Collector" for logic. A structural step in the process that specifically hunts for false equivalence, cherry-picking, and inertia.

The goal isn’t perfect rationality. That is impossible. The goal is consistent calibration.

A good team is a machine that ingests noise and emits signal.

eth2data.github.io

A journey through the underbelly of eth2’s final call before takeoff.

By Elias Simos and Sid Shekhar.

About this work: Elias is a Protocol Specialist at Bison Trails. Sid leads Blockchain Research at Coinbase. This report was an independent collaborative research effort to review the overall performance of the Medalla Testnet, answering the EF’s call for submissions on the eth2 Medalla data challenge (won silver).

All data, scripts, and notebooks that powered this analysis are available on github. The majority of the data we used came from the Prysm API via beaconcha.in.

The Honey Badger and the mirror

Adapted from an internal memo drafted in May 2019.

Bitcoin’s volatility profile is - by now - the stuff of legends. Monumental, euphoric rallies give way to abrupt, violent crashes and proclamations of Bitcoin’s demise (380 and counting). Thus far, the cycle has repeated without failure, earning Bitcoin the “Honey Badger” moniker in the process.

As the current cycle is unfolding, behind the BTC/USD pair’s most recent gyrations, new types of participants are entering the market; traditional macro money managers (e.g. PTJ) and nation states (e.g. Iran) are becoming increasingly open about dipping their toes in the cryptoasset ecosystem.

With every new type of player that jumps on board, the likelihood of Bitcoin becoming a widely accepted store of value and the Bitcoin blockchain becoming a globally accepted settlement layer, increases. The “why” Bitcoin makes for a good settlement layer and store of value has been covered extensively. However, the “how we get there” remains somewhat elusive. In this post, I will attempt to unpack that.

Fair != Equal

Let's for a moment imagine what an optimal state of the Bitcoin network at maturity looks like; Bitcoin is a widely accepted global store of value and/or settlement layer; global institutions (e.g. central banks) are on board, co-existing with crypto-native actors (e.g. miners); market manipulation is too expensive to attempt, as are direct attacks on the network; BTC is distributed widely among holders, such that network participants extract maximum value by being able to settle with all other parties they may wish to, and that no party has disproportionate “bargaining power” over network outcomes, allowing participants in the network to be continuously incentivized to remain participants.

From the above, a “fair” allocation of BTC among holders seems to be a key underlying requirement for this future to come to bear. Note that “fair” is not the same as “equal”.

Fairness, in this case, implies that every participant’s utility function is maximized, subject to their unique constraints. Under that condition, “equal” is “unfair” and therefore, unsustainable.

If we assume the “fairness” condition as requisite, then while not necessarily an easy pill to swallow, the rollercoaster ride might be the *only* path available to get us there. To illustrate the point, an approach by deduction reveals why the competing approaches cannot work;

A centrally planned diffusion mechanism: this construct fails as the planner holds all the bargaining power - such that no other party would willingly opt-in. In order to be executed effectively, it would have to be orchestrated and delivered by a benevolent dictator (a party with perfect information and perfectly benign incentives), and for all participants in the network to trust that the allocator is indeed benevolent. In practice, impossible.

A diffusion mechanism planned by a “political” coalition: this can’t be orchestrated in a multi-party explicit negotiation format, because there are too many conflicting interests at play in order to implement top down consensus. If it is sufficiently hard to achieve with structures where there is some cultural cohesion (e.g. EU and the Eurozone), it should be near impossible to achieve at a global scale.

So if we agree that neither of the two are viable options, the only option left is a free market mechanism; a continuous game, that is played by individualistic agents with hidden preferences, in near infinite (and infinitesimal) rounds, that allows for each participant to opt-in at the valuation that perfectly satisfies their objective function (what they strive to maximize under given constraints), therefore covering the full utility spectrum of the population of agents.

Hidden preferences become revealed ex-post and as such competing agents cannot devise a strategy that creates a surplus for themselves that leaves others at a deficit ex-ante, resulting to an ultimately fair distribution. And in the process of revealing preferences in a continuous game with infinite rounds, bubbles are created. Competing agents with similar objective functions are forced to respond to the first mover among their counterparts and jump on the bandwagon. Under scarcity, the price rallies, until the reservation price of agents that opted-in earlier is met. At that point the distribution phase begins, as earlier participants divest and get rewarded for stewarding the network thus far, by locking in a margin. As painful as the process might be, it ultimately yields to a fairer allocation.

As the "rounds" of the tacit negotiation - come free-market-bonanza - game unravel, the very nature of the platform evolves, opening up to a wider possible utility spectrum. With time, the network becomes more secure as wider margins become available for miners (either through higher prices or through advances in operational efficiency) and more resources are committed towards Bitcoin’s Proof of Work. It follows that as the network’s security improves, it opens up to new types of agents that are striving to maximize value preservation potential, subject to the liability they have to their constituents (measured as risk). The more types of agents there are on the network, the better a settlement layer it becomes, and so on.

Therefore, there is sense to the idea that progressively larger agents would opt-in at a higher prices, as they are effectively buying into a fundamentally different - and arguably better - network for value store and transfer. And with every new type of agent unlocked, the bandwagon effect re-emerges.

Bitcoin might not have been a secure or wide enough network for Square (an agent to its shareholders) to consider as its future payment rails and settlement layer in 2015. It is in 2020. Similarly, while Bitcoin might not be a secure or wide enough network for a sovereign to opt-in in 2020, it might be in 2025.

So, not only should we not be surprised by the new type of participant that is emerging in the early innings of this cycle, but we should expect more of this as the network’s value increases and its security profile improves.

And in the process, we should learn to accept the nature of the game.