Your Custom Text Here

Statefulness and value capture

One of the themes that has really stuck with me from the past couple of weeks on the road, is the idea that "tokens that govern state will accrue value, while tokens that govern schema won't". Here, I am looking to unpack this argument, touching on topics of statefulness vs statelessness, governance and value sinks. We'll start by understanding what statefulness is in a software context.

Stateless vs Stateful

State is the bulk of information referring to preceding events or user interactions, stored in a protocol (or programme) from t=0 up to t=n. A computer program stores data in variables, which represent storage locations in the computer's memory. The content of these memory locations, at any given point in the program's execution, is called the program's state.

By extension then, a stateless protocol does not require the server to retain session information or status about each communicating partner for the duration of multiple requests. Examples include the Internet Protocol (IP), which is the foundation for the Internet, and the Hypertext Transfer Protocol (HTTP). Conversely, a program is described as stateful if it is designed to remember preceding events or user interactions. In stateful protocols, information about previous data characters or packets received is stored in variables and used to affect the processing of the current character or packet.

Statelessness imbues software with fast performance, reliability, and the ability to grow, by re-using components that can be managed and updated without affecting the system as a whole, even while it is running. In contrast stateful protocols, provide continuity and are more intuitive (since state related data are embedded).

Statefulness and value over time

Blockchains and smart contracts platforms, are in their majority, stateful. By definition, a blockchain is a database of past states - such that the further away we move from t=0, the more stateful it becomes. This is equally true for Web 2.0 systems, but especially true for blockchains.

Consider the following example: a user may interact with the service to address a personal need, for example, to find a certain website with the aid of a keyword query. The service satisfies that need by returning a list of results, but a byproduct of the user’s action is the service improving its global state - e.g. with every new search queried, Google's algorithm is more informed than before, and therefore better able to deliver optimal results for all future users.

So it appears that while code is of paramount importance to kickstart a software system, as time goes by, the value migrates from the code to the state captured by the programme/protocol. A service’s reliance on state makes it fundamentally different than a tool. A service’s software, when instantiated, creates a vessel for persistent state. It starts off empty and becomes useful only when filled with data, users or both. State compounds and becomes more valuable exponentially. Code, while crucial for the stable operation and evolution of a service, becomes less important and necessary to defend.

As Denis Nazarov of a16z has noted in the recent past, "blockchains are too slow to do any computing that is really interesting aside from their one redeeming feature: they maintain “state” incredibly well", while concluding that they are probably the best “state machine” invented to date — properly aligning the incentives to coordinate a network of machines distributed globally that maintain this state of truth without an intermediary.

Statefulness and value capture

So, from the above, it follows that (i) stateful protocols have memory; the more memory they accumulate, the more valuable they become and (ii) value migrates from code to state over time. At the same time, (iii) the more memory stateful protocols and apps accumulate, the slower they become and (iv) blockchains are the best state machines invented to date.

Granted all of the above then, is there truth to the statement - "tokens that govern state will be valuable, tokens that govern schema won't"?

Since blockchains are in effect databases, we can define schema as the overall design of the database - the skeleton structure that represents the logical view of the entire database. It tells how the data is organized and how the relations among them are associated. Conversely, as mentioned previously, state refers to the content of a database at a moment in time.

It then follows that as governance of an open source system comes into place, the value accrues increasingly more to the ability to influence future state. In other words, having influence over the terms that influence state (e.g. Maker DAO liquidation margins) is more valuable relatively to having influence over how those terms come into effect.

A dive into Ethereum's network stats

Taking from Chris Burniske's recent post on crypto fundamentals (especially ETH's) being less depressed in protportion to ETH's USD denominated value, I did some digging on the fundamentals of ETH beyond Gas and hashrate. In today's version of the Daily, I'll present you with some key metrics on Ethereum and attempt to unpack where the state of the network is at present.

Key Takeaways:

The Ethereum network seems to have reached a capacity ceiling in its current form.

Smart contract usage is correlated to relative transaction cost.

ERC-20 is by far the dominant standard.

Poor quality ERC-20's are starting to go offline. That should allow for some network bandwidth to free up.

High quality smart contract useage is accelerating. That is likely to increase the demand for bandwidth - as organic (non-speculative) demand kicks in.

13% of all available ETH is currently locked in Maker DAO. That's an impressive feat, a sign of progress, and a HUGE central point of failure.

Without a scalability solution, the problems that became evident in 2018, will only keep persisting, as adoption of the platform increases.

Exhibit 1: The network has reached a capacity ceiling

These two plots are directly borrowed from Burniske's post and show the relationships between Market cap (Network Value) and daily transactions and hashrate respectively. Safe to make the case that the network holds its relative fundamental strength, despite the price of ETH collapsing. There are a few cases we can make here. The most interesting ones to me are (i) the fact that mania pushed the valuation much higher than the fundamentals, but more interestingly, (ii) the fact that the market is pricing in Ethereum's scalability woes. Plasma is starting to look like a Catch 22, Sharding is being continuously delayed and the Ethereum community has grown bigger than its current organizational structures can accommodate. Be that as it may, the fact that both hashrate and daily transactions have plateaued in 2018, remains. The next couple of graphs show the effects of the network bottleneck, in action.

The two graphs above are representations of smart contract count and the relative transaction cost (measured as Gas value/ETH value). Just a quick glance in enough to reveal that there is an negative correlation between the two constructs. Low relative transaction costs lead to proliferation of smart contracts deployed on Ethereum. Fair. What is positive here is that despite the windfall in ETH's value, we recently hit a local maximum in smart contract count. The flow of developers on Ethereum is increasing - yet, they are likely to find themselves competing for finite resources. Let's take a look on the demand side of those smart contracts.

Exhibit 2: Smart contract usage is correlated to relative transaction cost

The plots above are different permutations of smart contract calls over time. A smart contract call is similar to an API query. As evidenced by the number of unique callers over time, the Gas crisis this past summer (largely attributatble to Fcoin's introduction of trans fee mining), capped the growth of unique callers. Even as transaction costs normalised, the number of unique callers did not return to its previous trajectory. A look at the number of calls might reveal why;

The capacity ceiling in Ethereum's current form becomes evident once more. Call count has plateaued at 300k for pretty much all of 2018. When calls started reaching 400k, transaction fees blew up and the call count returned to the 300k level. The fact that many useless ERC-20s are starting to die out, some capacity should be freed up. Even yet, were this source of demand to be substituted with real users, we can expect that the same mechanics would come into play.

Exhibit 3: ERC-20 is by far the dominant standard

Recently, the number of daily unique ERC-20's in operation took a turn south. The recent drop in the number of ERC-20's coincides with the recent actions from the SEC. Even so, their overall share of the Ethereum network is so large, that makes the traction of other ERC standards (like the NFT - 721) pale in comparison. Still; in relative terms the signs of life in non-fungibles and others are encouraging.

Interestingly, the number of daily transactions of ERC-20's has been on the decrease since July, coinciding with the aforementioned Gas crisis that took place around that time. Part of this change might be attributable to some of the demand sources moving to other platforms and some dying out due to continuously depreciating prices. But there's potentially one more reason...

Exhibit 4: Open Finance Dapps like Maker are starting to get serious traction

The trend change in daily transactions of ERC-20's, as well as the number of smart contract callers, coincides with an acceleration in the trend of increase of the amount of ETH that is stored in the Maker DAO smart contract, held as collateral to issue the DAI stablecoin. At the moment, approximately 13% of the available supply of ETH is locked into that contract (no wonder a16z piled in ~$25M in Maker), while others smart contracts, such as Compound, have started gaining traction (on display in the second graph above).

Concluding remarks

That final point is perhaps what's more encouraging about the ecosystem's development. More is not always better. The evidence that the number of ERC-20s is starting to drop, while high quality smart contracts are accelerating in useage is a highly positive sign, and a trend that we can only hope persists in 2019. However, without a robust scalability solution, the woes of the past are almost certain to keep coming back as demand picks up - and demand from builders for the Ethereum platform shows no signs of slowing down.

Monthly downloads of the Truffle development framework for Smart Contracts

To top that up, the Maker smart contract is increasingly becoming a bigger and bigger bounty for the one to hack it, and a central point of failure for the whole Ethereum ecosystem. Useful to remember that Solidity (Ethereum's programming language) comes without formal verification, and thus higher probability of bugs appearing down the line. So far, so good - but then again it doesn't matter how you fall - what matters is how you land.

The king is naked

The Diar has recently published some data on the treasury balances of ~100 crypto projects' ICO wallets, and I thought it would be interesting to run a few analyses on the data and see what sort of insights (if any) we can elicit. Before we dive in, it's useful to note that the projects examined here only represent 5-10% of the whole. There is a multitude of other projects that are not included in this dataset - or any other publicly available dataset as far as I know. If you happen to know of a more comprehensive resource, do get in touch. Now without further ado, let's get to it;

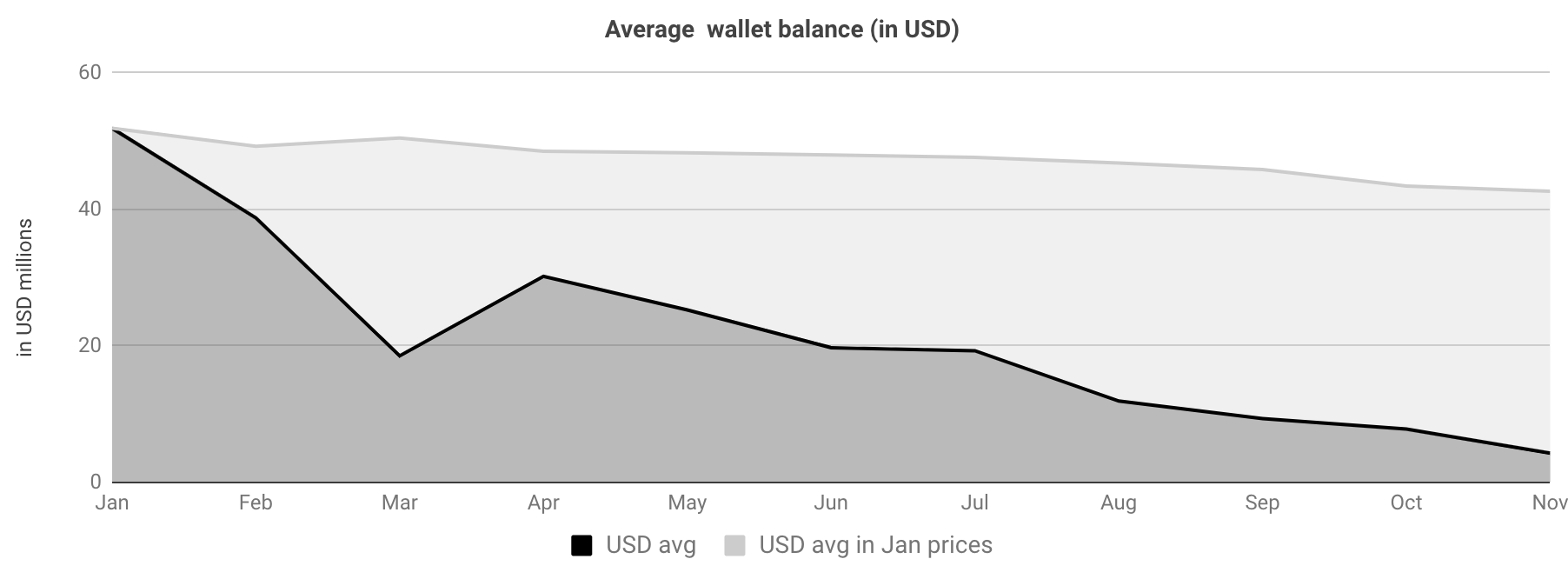

The first figure shows the total ETH balances in the projects' wallets and how that figure has been shaped over the course of the year. The total wallet balance has decreased by 17.8%, while ETH's price has decreased by ~90% from January 2018. Putting two and two together, this amounts to a 92% decrease in the USD value of those holdings. In absolute terms, the average project's treasury, lost about $38M in potential value held, since January - see figure below.

Theis is a summary of the simple average size of a random project's treasury, accross 2018, expressed in USD terms. The dark area represents the actual value of the treasury, while the light shaded area, represents the value lost due to ETH's price depreciation. In order to highlight the degree of potential mismanagement, let's run a quick thought experiment; starting out in January 2018, project ABC has $55M in its treasury. Let's also assume that the optimal budget distribution for ABC, looks something like what's presented below.

The above implies that ABC can hire approximately 60 professionals (engineers, ops, marketing), at Silicon Valley salaries (~$180k a year average), and keep them employed for 3 years. While I don't have concrete numbers on this, last time I checked, most projects that raised in 2017 are not on a hiring spree of that magnitude. Let's further assume that ABC actually consumed 17.8% of the $55M they raised (approx. $10M), out of which $5M is committed towards payroll (by the above assumptions). With that they hired 9 people, which sounds about right. Now, had they managed their finances optimally, they would still have enough money to hire another 50 people to help them build and ship. What the reality points to is that they can actually hire about 3 more people at SV salaries and keep them employed for 3 years. That's a tentative loss of 47 high quality professionals. Wow! Surely there was no CFO among those 9 hires that ABC went ahead with in 2018...Note that we are talking about are technology organizations that have raised money to deliver a product/network - not finance shops. As such I don't see how they can justify being long ETH.

Now let's have a quick look at how the total ETH liquidation activity relates to the price of ETH.

The correlations here are not very revealing; there is a positive 30% correlation (relatively weak) between this month's ETH liquidation and next month's %D in the price of ETH and a negative 40% correlation between this month's ETH liquidation and this month's %D in the price of ETH . In other words, there is some correlation between projects selling ETH and the price of ETH dropping, but it seems to not be the most compelling reason why. Again, we are only tracking ~5% of all projects here, so there is a chance that the correlations would increase if we had a more complete picture.

To round off the analysis, let's take a look at how specific projects have managed their treasuries thus far.

The dark area signifies how much the project's treasury was worth in USD terms in January, while the the light area represents the % of the treasury that the project consumed (or liquidated to USD). There are a few key observations here; (i) the distribution between total value in January and amount consumed is random, (ii) the amount consumed has not impacted price overall (for most projects) - one would assume that better management would translate to the market pricing that in and (iii) some of the most hyped projects, like Tezos and Golem, have consumed none of their ETH holdings in 2018.

There are a few conclusions that really stand out here; (i) the average project has no idea how to or low interest in managing their treasury and part of that lack of activity is most likely owing to the fact that (ii) in 2017 projects raised way too much money, compared to what they needed to ship product. It would also appear that (iii) many of the teams succumbed to the whims of an anchoring bias, and while the USD value of their ETH holdings 2-5xed over the course of 2017, they didn't bother to liquidate some, as that was way over the amount that they initially asked for. Of course, this is something that we already knew, but interesting to see how it has played out over time. This abundance of (notional) capital, surely did not create an optimal incentive structure for the teams.

As the industry matures, the need for diverse skillsets is evident, as is the current lack of design and ops/finance people in crypto - despite the increasing flow. While there are many things wrong with the "real world" that crypto has the potential to improve, there are equally many things done right, that crypto would be better off adopting.

The stablecoin paradox

The more I study emerging stablecoin propositions, the more convinced I become that this is an all-or-nothing market. Unless you have absolute conviction that one design will win, it makes little sense to back any single stablecoin at all.

This isn’t like betting on competing tech platforms where several can coexist. Stablecoins fight for the same narrow space: trust, liquidity, and exchange integration. Every new entrant dilutes the rest, pushing the market toward a single dominant winner.

Stablecoins are also an exceptionally risky business. Beyond the operational fragility of many designs, the value-capture mechanisms that link a stablecoin to its governance token are often murky. Add a hyper-competitive market with almost no barriers to entry, and you have a setup where each new launch erodes the future value of all others. Since early May, when I first started tracking the space, the number of live or planned stablecoins has more than doubled (see stablecoinindex.com for a running list).

This will almost certainly be a winner-takes-most market.

Take the current leader, Tether. Many projects have tried to unseat it, yet none have come close. What’s remarkable is how little effort Tether has made to polish its image—no full audit, constant skepticism—and still, it dominates. Why? First-mover advantage and attention.

Attention converts to revenue. Claiming attention real estate early can make or break a company. Tether might be one implosion away from collapse, but time compounds its advantage: it gets smarter, more entrenched, better resourced.

Now imagine two plausible dethroning scenarios:

Collapse: A revelation shows only 10% of Tether’s supply is actually backed by dollars.

Institutional flood: Tens of billions in institutional capital enter crypto, flowing into the most transparent, regulated alternative.

In either case, the market would reshuffle briefly before a new stablecoin king emerges. The logic mirrors why the world runs on the USD: attention, liquidity, and interoperability. We don’t deal with USD #1 through USD #99. We deal with the USD.

If I had to bet, I’d back the institutionally backed, fully regulated alternative. As the market matures, institutional participants will favor systems that resemble those they already trust. Their adoption would cascade, signaling legitimacy and pulling the rest of the market along.

The arrival of Gemini Dollar and Paxos Standard marks exactly that kind of shift—a sign that crypto is inching toward maturity.

Message from the future: As fate would have it, Circle with USDC would go on and carve its own space in the category.